KUALA LUMPUR: Mah Sing Group Berhad (“Mah Sing”), a prominent Malaysian property developer, continues to exhibit robust performance, driven by strong demand for affordable housing and strategic expansion into the data centre (DC) sector.![]()

Strong Financial Performance in 1HFY24

Mah Sing reported a core net profit (CNP) of RM116 million for the first half of the fiscal year 2024 (1HFY24), marking a 19% year-on-year increase. This performance came despite a 12% decline in revenue, attributed to the early stages of new project sales that have yet to significantly contribute to the company’s top line. The improved CNP margin, rising to 10% from 7.5% in the previous year, underscores the company’s effective cost management and project execution.

Affordable Housing Segment Remains a Pillar

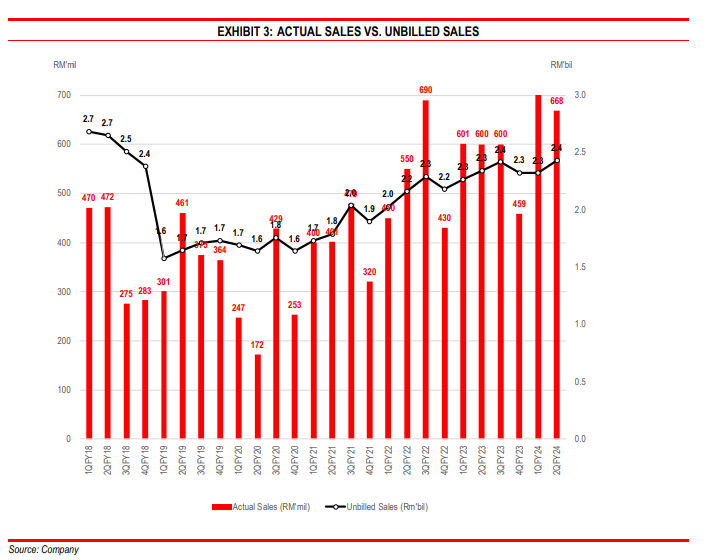

The company has secured RM1.7 billion in new sales year-to-date, achieving 66% of its FY24 sales target of at least RM2.5 billion. This success is largely driven by the affordable housing segment, which continues to see over 90% take-up rates. With multiple project launches planned in the second half of the year, including M Aspira, M Terra, and M Zenya, Mah Sing is well-positioned to exceed its sales targets.

Strategic Expansion into Data Centres

In addition to its property development business, Mah Sing is making significant strides in the data centre sector. The initial collaboration with Bridge Data Centres for up to 100MW capacity at Southville City has set the stage for further expansion. The company is currently in advanced negotiations for an additional 90MW project and is exploring the sale of 42 acres of land at its Meridin East township in Johor Bahru to a data centre player. This move could generate a disposal gain exceeding RM100 million, contributing significantly to Mah Sing’s FY24 net profit.

Outlook and Valuation

AmInvestment Bank has maintained its “BUY” rating on Mah Sing with an unchanged fair value of RM2.11 per share, based on a sum-of-parts (SOP) valuation. The stock trades at a price-to-earnings (P/E) ratio of 14x for FY25, offering a fair dividend yield of 3%. The bank’s positive outlook is supported by Mah Sing’s agile business model, strong focus on affordable properties in high-demand areas, and strategic foray into Malaysia’s booming data centre industry.

As Mah Sing continues to leverage its core competencies and explore new growth avenues, the company remains well-positioned for sustainable long-term growth, backed by strong financials and strategic initiatives.

Analysts’ reports maintain BUY call on Mah Sing respectively:

- UOBKayHian – 2Q24: Results Within Expectations; Achieves RM1.66b In Sales (TP: rm2.29)

- TA Securities – Steady Performance (TP: RM2.11)

- RHB – Awaiting More DC Deals To Come; BUY (TP: RM 2.26)

- CIMB Securities – 1H24 results inline; DC plans taking shape (TP: RM2.10)

- AmInvestment Bank – Robust demand for affordable homes with DC catalysts (TP: RM2.11)