KUALA LUMPUR: The Malaysian property sector has garnered significant attention, as RHB Investment Bank maintains its Overweight recommendation for real estate amidst key macroeconomic shifts and impending policy decisions. This positioning reflects optimism surrounding the economic landscape and the opportunities it presents, particularly with the prospect of rate cuts by the US Federal Reserve. RHB’s latest report outlines the factors contributing to a promising outlook for developers, institutional investors, and property buyers alike.

Impact of Interest Rate Cuts on Real Estate

![]()

As the US Federal Reserve enters a rate-cutting cycle, regional institutional funds are expected to channel more capital into real estate, marking Malaysia as a prime destination for such investments. Falling interest rates generally bode well for property markets, offering attractive borrowing costs for developers and buyers. The stabilizing Malaysian Ringgit (MYR) and interest rates further amplify this appeal. As institutional investors regain confidence, the local market may see a surge in demand for high-growth properties and strategic locations.

Malaysia’s property sector has seen renewed interest, with particular focus on data center (DC) investments, as the country’s strategic location makes it a hub for such assets. Recent high-profile sales, such as the sale of AirTrunk, the largest DC group in the Asia-Pacific, for AUD24 billion (USD16 billion), showcase the global demand for digital infrastructure, bolstering investor confidence in Malaysia’s burgeoning DC sector. Local developers, such as Sime Darby Property (SDPR) and Mah Sing, stand to benefit from this global trend .

Potential Growth in REITs

Falling interest rates are not only favourable for traditional property investments but also for Real Estate Investment Trusts (REITs). As more developers contemplate REIT listings, particularly those with significant portfolios of investment properties, the sector’s dynamics could shift toward greater monetization of assets. Companies such as IOI Properties and SP Setia have already considered this route, and SDPR is emerging as a prime candidate given its expanding portfolio, which includes KL East Mall, Senada Mall, and Elmina Lakeside Mall. With the completion of Google’s data center in 2026 expected to add MYR1.5–2 billion to its portfolio, SDPR could witness substantial valuation growth .

Iskandar Malaysia: A Key Market Driver

The Iskandar Malaysia region remains a significant driver of property demand, with several catalysts fueling this growth. The upcoming Rapid Transit System linking Johor Bahru and Singapore, alongside potential investments through the Johor-Singapore Special Economic Zone (JS-SEZ), positions Iskandar as a hotbed for both foreign and local investors. This renewed interest is already visible, as developers such as UEM Sunrise and Sunway report strong demand for their launches in the region .

For instance, UEM Sunrise’s recent soft launch of Direka Square shop lots and Sunway’s Maple homes saw 3–4 times oversubscription for pre-launched units. Additionally, buyers from Singapore accounted for 20% of the pre-sales for Sunway’s projects, underscoring the region’s attractiveness to cross-border investors .

Key Projects on the Horizon

Looking ahead, several major developments are poised to shape Malaysia’s property landscape:

- Budget 2025: Scheduled for next month, it is expected to introduce measures that may further stimulate the property sector, particularly with favorable policies for industrial developments and affordable housing.

- Kuala Lumpur-Singapore High-Speed Rail (HSR): The potential revival of this ambitious project could reignite demand for properties along the route, benefiting developers with exposure in these areas, such as UEM Sunrise and Sunway .

- Special Economic Zone (SEZ): The Johor-Singapore SEZ, with its influx of foreign direct investments (FDIs), is anticipated to spur further real estate transactions in the Iskandar region.

Developer Recommendations and Valuations

In light of these favorable conditions, RHB Investment Bank has identified its top picks in the property sector:

- Sime Darby Property (Target Price: MYR2.00, 33.9% upside)

- Mah Sing (Target Price: MYR2.26, 32.7% upside)

- UEM Sunrise (Target Price: MYR1.60, 63.7% upside)

- Sunway (Target Price: MYR5.00, 14.1% upside)

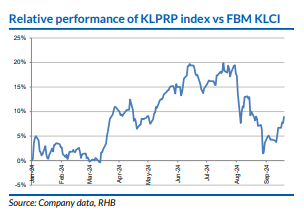

These developers, with their exposure to both residential and industrial real estate, are well-positioned to capture the opportunities emerging from Malaysia’s evolving property market. The overall sector trades at a 48% discount to Realizable Net Asset Value (RNAV), presenting attractive entry points for investors .

Conclusion: An Optimistic Outlook

As Malaysia transitions into a lower interest rate environment, its real estate sector is set for robust growth. Developers, institutional investors, and individual buyers are likely to benefit from favorable macroeconomic conditions, renewed investor interest, and strategic government policies. With key projects on the horizon, including the revival of the HSR and the development of the JS-SEZ, the property sector offers substantial potential for both local and international players.

The Overweight rating by RHB underscores this optimism, reinforcing Malaysia’s position as a prime destination for property investments in the region.