KUALA LUMPUR: The Malaysian property market continues to grapple with significant challenges such as oversupply, high household debt, and affordability concerns. According to Kenanga Research’s October 2024 sector update, the outlook remains underweight, especially for larger developers whose stock performance is underwhelming. Despite these headwinds, mid-to-small-cap developers in the industrial and land sales segments are providing a stabilizing cushion amid the turbulence.

Key Drivers of Stability: Industrial and Land Sales

Industrial property and land sales are emerging as more resilient business models, driven by growing demand from sectors like e-commerce and logistics. Developers like MAHSING and Sime Darby Property are shifting focus towards these segments, which offer a reliable revenue stream compared to the beleaguered residential market. This strategic pivot allows developers to mitigate the risks posed by the affordability crisis and oversupply in the housing market.

Government initiatives to attract foreign direct investment (FDI) have further bolstered industrial property demand, making it an area of growth even as other property sectors face stagnation.

Residential Sector: Oversupply and Affordability Crisis

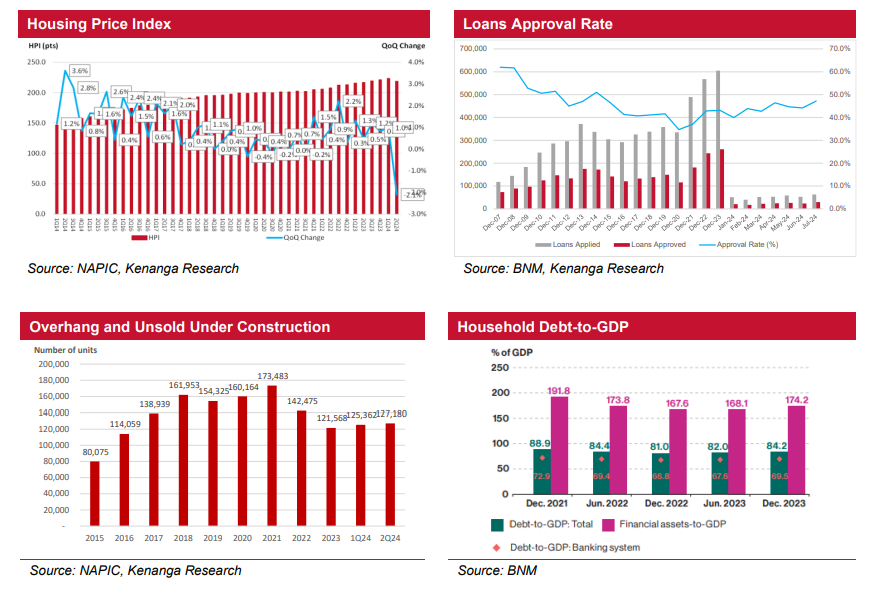

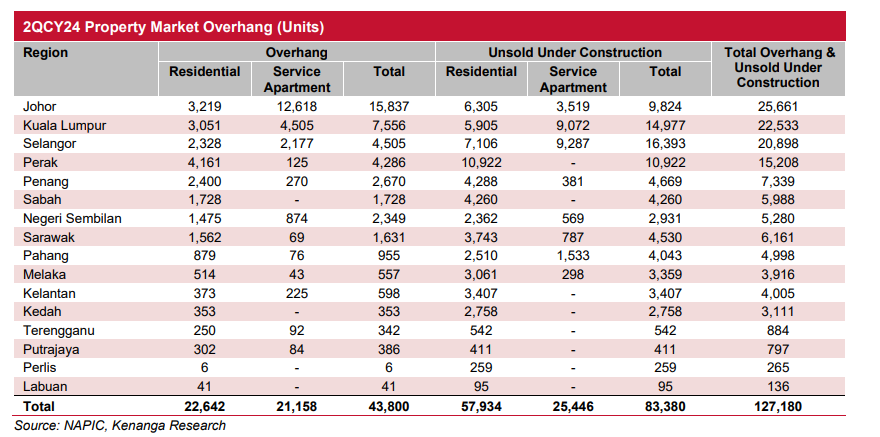

The residential market continues to face an oversupply, with overhang units rising to 127,180 as of 2QCY24, a 3% increase from the previous quarter. This is compounded by rising household debt-to-GDP ratios, which have increased to 84.2% in 2023 from 81.0% in 2022, yet remain below pre-pandemic levels. While housing loan approval rates have improved to 47.2%, this improvement is largely in the affordable housing segment, where developers are targeting properties priced below RM500K.

Despite efforts to provide affordable housing, younger Malaysians—particularly first-time homebuyers under the age of 35—are struggling to secure home loans. The gap between the median house price of RM335K and average monthly salary (RM3,000-RM3,500) makes homeownership unattainable for many, even in the affordable housing category. This has left many units, particularly those priced below RM300K, unsold, with the highest concentrations of overhang units in urbanized regions like Johor, Kuala Lumpur, and Selangor.

Economic Outlook and Sector Resilience

Inflationary pressures, particularly the potential rationalization of the RON95 fuel subsidy, could dampen consumer sentiment and spending power, which would further strain property demand. However, the appreciating Malaysian ringgit offers a silver lining, potentially easing some of the cost burdens for developers and consumers alike. Additionally, the stabilization of the Overnight Policy Rate (OPR) at 3.00% has reduced market uncertainty, offering some respite from earlier interest rate hikes.

Developers are increasingly focusing on monetizing land near developed areas and prioritizing affordable housing projects. This strategic shift has allowed for some level of resilience, even in the face of persistent economic headwinds. The growth of transit-oriented developments in regions like the Klang Valley is also expected to gain momentum, providing a strategic response to rising living costs and household debt pressures.

Top Picks and Future Outlook

Kenanga Research’s top sector picks include MAHSING and MKH, both of which focus on affordable homes and transit-oriented developments that align with shifting consumer preferences. In contrast, Malaysian Resources Corporation Berhad (MRCB) was downgraded to Market Perform from Outperform due to its valuations catching up with its construction-driven growth prospects.

In conclusion, while the Malaysian property sector faces considerable challenges, industrial property and land sales offer a reliable cushion. Developers’ shift toward more sustainable revenue streams, along with targeted strategies in affordable housing and landbank monetization, may help them weather the storm. However, the affordability crisis remains a significant issue, calling for more targeted interventions to resolve the growing overhang of unsold units.0