SINGAPORE: In its Asia-Pacific Logistics Markets report for H1 2024, leading independent global real estate adviser Knight Frank says rental rates for logistics spaces in the region have sustained their upward trend. However, this growth has occurred at a more moderate pace compared with previous periods.

The region recorded an average year-on-year rental growth of 2.4% in H1 2024, marking a significant slowdown from the 6.2% increase observed in 2023.

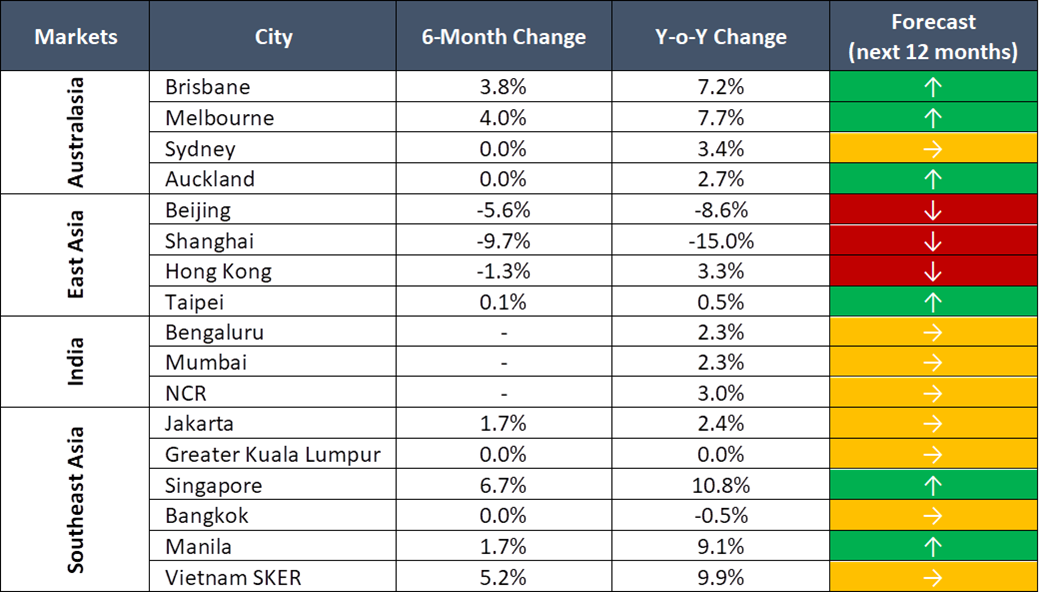

Singapore emerged as the standout performer in the region, with logistics rents increasing 6.7% from six months ago and 10.8% year-on-year, the highest growth recorded in ten years.

Singapore’s strong manufacturing led the growth, with the Purchasing Managers’ Index expanding consecutively over the last 10 months. This strong performance is expected to continue, with forecasts projecting a 3% to 5% increase in prime logistics rents for 2024, as international manufacturers continue to view Singapore as an attractive location for their overseas operational expansion plans.

Despite the overall positive trend, 14 out of 17 tracked cities in the region recorded stable or increasing rents year-on-year in H1 2024, a marginal improvement from six months ago. This indicates a broader pattern of growth across most markets, even as the pace moderated.

Tim Armstrong, global head of occupier strategy and solutions, says, “Global supply chains have again contended with disruptions this year, which have lifted transportation overheads. Consequently, margin pressures have continued to remain significant amid weaker consumer demand. Most occupiers are also anticipating higher rental rates on lease renewals. Constrained by the fragile economic outlook and challenging operating conditions, occupiers will continue to scrutinise space requirements. Leveraging technology and strategically aligning logistics footprints will remain key priorities. Occupiers are expected to be increasingly discerning when considering expansion spaces.”

The slowdown in rental growth was primarily attributed to challenging conditions in Chinese Mainland markets, particularly Beijing and Shanghai. A slowdown in business activity led to a significant 13.5% decline in rentals, with vacancy rates climbing to over 20%. This has prompted landlords to implement rental reductions and offer shorter lease terms in an effort to attract and retain tenants.

Christine Li, head of research, Asia-Pacific, Knight Frank, says, “Although conditions in Beijing and Shanghai are sharply in contrast with the rest of the region, still, it remains clear that logistics occupier markets are on the whole transitioning to a more neutral state from one favouring landlords. However, despite moderating demand, the long-term fundamentals supporting the region’s logistics space market remain intact. As supply chains shift, manufacturing is emerging to be an important sector driving logistics development, along with e-commerce and 3PL players. While there will be ample flight-to-quality options in Beijing and Shanghai, these markets will remain under pressure until adsorption capacity picks up.”

Market performance and forecast for the next 12 months: